As global demand for electric vehicles and energy storage continues to surge, the battery industry is entering a new phase of innovation. Amid concerns over lithium price volatility, supply chain resilience, and performance in extreme climates, sodium‑ion batteries are emerging as a compelling complementary technology to lithium‑ion systems.

1. Why Sodium‑Ion Batteries Are Back in the Spotlight

Although sodium‑ion battery research dates back to the 1980s, the technology has recently regained traction thanks to rapid advancements and growing industrial investment. Several factors are driving this renewed momentum:

- Superior low‑temperature performance Next‑generation sodium‑ion cells can retain around 90% of their capacity at –40°C, outperforming lithium iron phosphate (LFP) batteries in cold environments.

- Reduced exposure to lithium price fluctuations Sodium is abundant and widely distributed, offering a more stable and diversified raw‑material base.

- Accelerating industry adoption

- CATL has announced its second‑generation sodium‑ion battery and plans for mass production by 2026

- BYD has begun constructing its first sodium‑ion battery facility

- Companies such as Hina are introducing sodium‑ion solutions for electric mobility

These developments signal that sodium‑ion technology is transitioning from feasibility studies to early‑stage commercialization.

2. The Key Challenge: Energy Density Still Lags Behind

Despite its advantages, sodium‑ion technology faces a significant hurdle: lower energy density.

- Current sodium‑ion cells: ~175 Wh/kg

- LFP cells: ~205 Wh/kg

- High‑nickel NMC cells: up to 255 Wh/kg

This gap translates into shorter driving ranges. A sodium‑ion EV might achieve around 350 km, compared with 400–600 km for mainstream lithium‑ion models.

Additionally, while sodium‑ion batteries avoid lithium and graphite, they still rely on materials such as nickel and manganese — minerals whose processing remains geographically concentrated. As a result, supply chain risks are reduced but not eliminated.

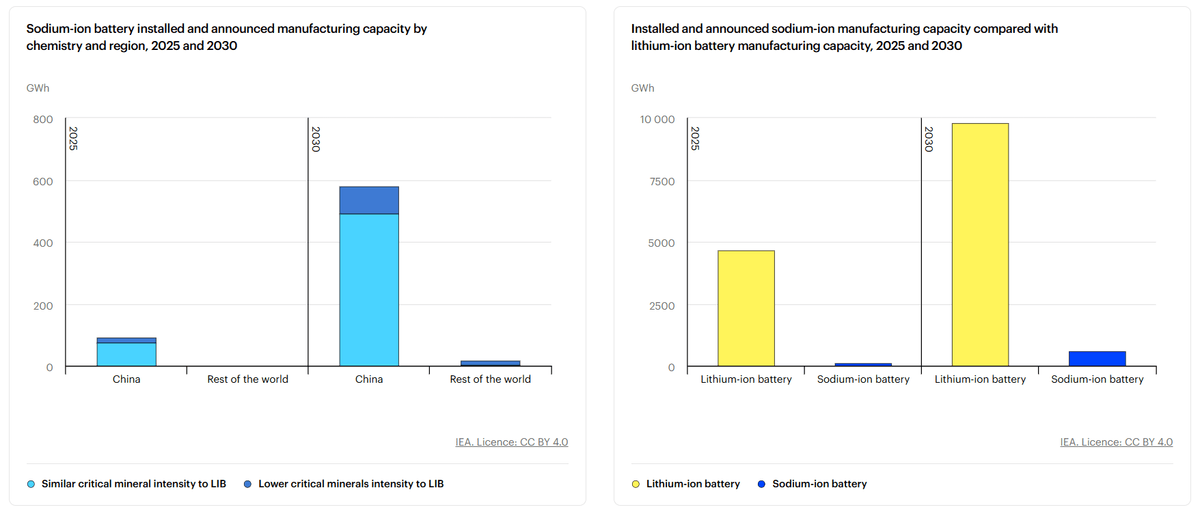

3. A Highly Concentrated Supply Chain: China Leads the Way

According to IEA data:

- 95% of global sodium‑ion battery production capacity — existing and planned — is located in China

- Most key materials, including cathode and anode active materials, are also produced by Chinese companies

This concentration highlights both the rapid progress of China’s battery ecosystem and the early‑stage nature of sodium‑ion development in other regions.

Source: International Energy Agency (IEA), used under CC BY 4.0. No changes were made. License: https://www.iea.org/terms/creative-commons-cc-licenses

4. The Future Role of Sodium‑Ion: Complementary, Not a Replacement

Sodium‑ion batteries are not positioned to replace lithium‑ion technology. Instead, they are expected to serve as a strategic complement in specific applications:

- Electric vehicles in cold climates

- Grid‑scale energy storage, where cost and cycle life matter more than energy density

- Hybrid lithium–sodium battery packs, where sodium cells can support low‑temperature discharge and reduce lithium‑ion degradation

The long‑term adoption of sodium‑ion batteries will depend on two major factors:

- Whether lithium prices remain elevated

- Whether sodium‑ion energy density can continue to improve

5. Our Perspective: A Valuable Step Toward a More Resilient Energy System

The rise of sodium‑ion batteries represents an important step toward diversifying global energy storage technologies. They offer new supply chain options, improved cold‑weather performance, and cost advantages for large‑scale storage.

However, achieving global scale will require:

- Continued breakthroughs in energy density

- A more geographically diversified supply chain

- Ongoing investment and international collaboration

In the evolving landscape of clean energy, sodium‑ion batteries will grow alongside lithium‑ion technologies, helping build a more flexible and resilient energy ecosystem.