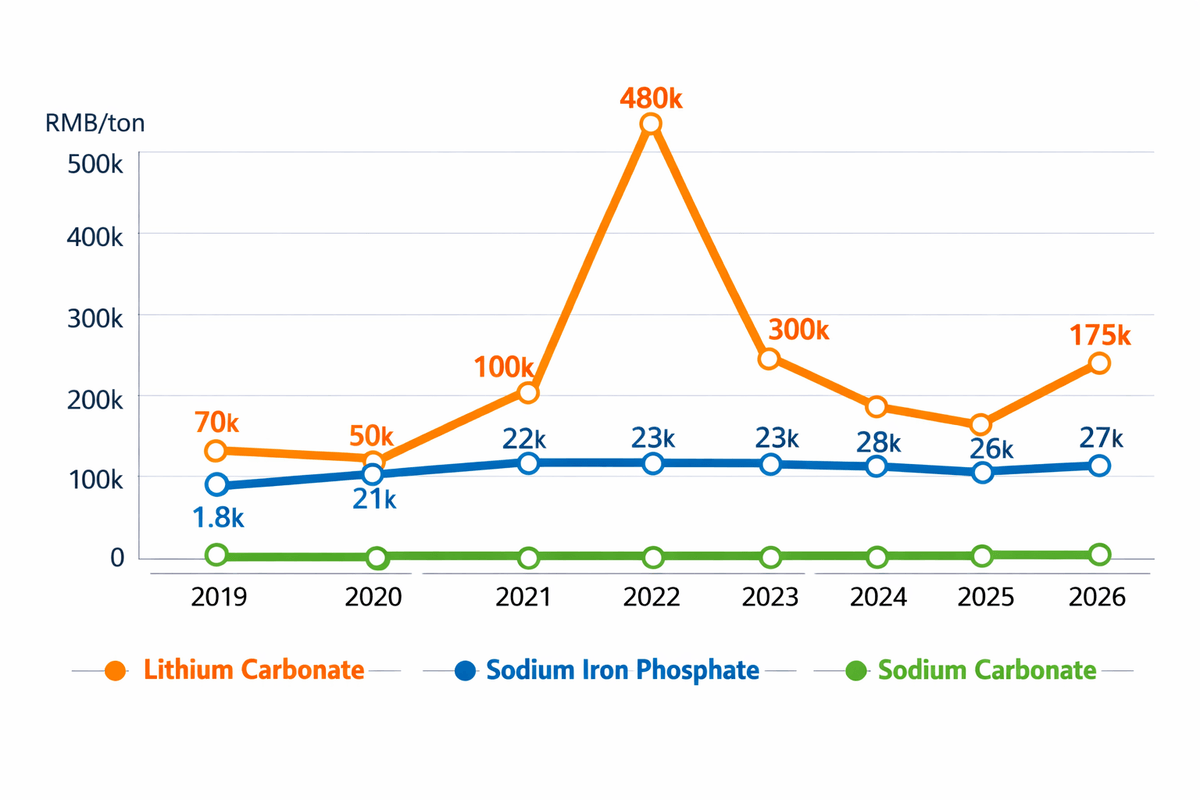

From 2019 to 2026, the global battery industry experienced dramatic shifts in raw material prices.By examining seven years of historical data for three key materials — Lithium Carbonate (Li₂CO₃), Sodium Iron Phosphate (NaFePO₄), and Sodium Carbonate (Na₂CO₃) — a clear pattern emerges: Lithium-ion batteries face extreme cost volatility, while sodium-ion batteries benefit from stable, low-cost raw materials.

This price divergence is reshaping the economics of energy storage and accelerating the rise of sodium-ion technology.

🔹Cost Comparison: How Big Is the Gap?

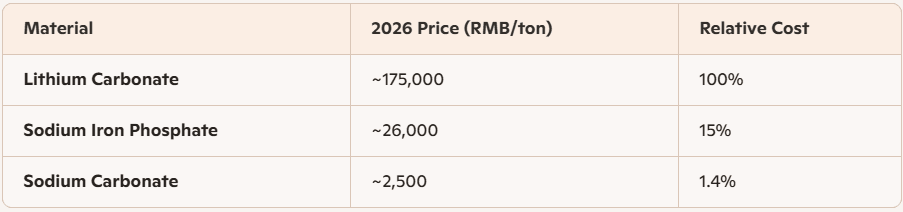

Sodium-ion raw materials are 6–70× cheaper than lithium-ion materials. And more importantly: Sodium-ion prices are stable. Lithium-ion prices are not.

🔹Why Sodium-Ion Prices Stay Stable

✔ Abundant resources

Sodium, iron, carbon, and phosphorus are among the most common elements on Earth.

✔ No dependence on scarce metals

No lithium, nickel, cobalt, or graphite bottlenecks.

✔ Mature global supply chains

Sodium carbonate and iron phosphate industries have existed for decades.

✔ No geopolitical concentration

Unlike lithium (concentrated in Chile, Australia, China), sodium resources are globally distributed.

🔹 Conclusion: Sodium-Ion Is Not an Alternative — It Is the Inevitable Complement

Based on seven years of historical data:

- Lithium-ion will continue to dominate high-energy-density applications.

- Sodium-ion will lead in cost-sensitive, large-scale markets such as:

- Grid storage

- Renewable energy buffering

- Telecom backup

- Residential storage

- Low-speed mobility

- Amost all use cases of LAB

The future is dual‑track: lithium for density, sodium for cost. And the 2019–2026 price curves already tell this story clearly.